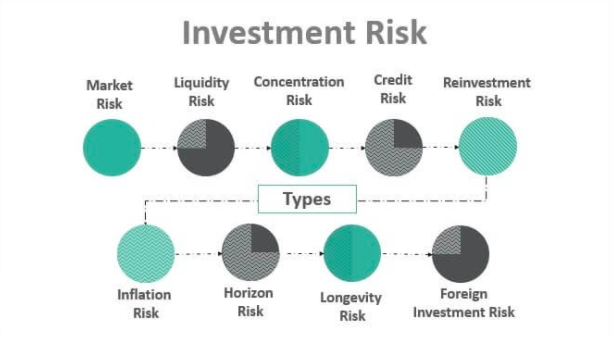

If you go to school to study finance you’ll learn about different types of risk. Here Threadgill Financial are sharing some of the major ones that affect stock prices.

Interest Rate Risk: if interest rates rise significantly. If that happens those who own stocks may prefer getting interest from CDs or bonds. For example, if you own an ATT that yields about 5.5% and interest rates rise so that you can get 5.5% on a CD, you might prefer the safety and certainty of the CD rather than from ATT. What one would give up with the CD would be a growing income. Dividends at ATT have been growing about 2% a year, while interest from a CD is flat.

Business Risk/Company Specific Risk: If your investment portfolio is too concentrated and one of your investments doesn’t work out, you might lose your principal. We address this risk by not being too concentrated. Statistics suggest that somewhere between 20 and 30 stocks is enough to diversify away most company specific risk. We typically invest in 30-40 companies.

Sector Risk: If the 30-40 companies we held were all in one sector and that sector had a rough patch, this could be a problem. Think tech stocks in the tech bubble, bank stocks in 2008-2009, and oil stocks in 2016. The S&P 500 is divided into 11 sectors. We usually own stocks in all several sectors, though at times one sector or another becomes more attractively priced and we might tilt that direction.

Market Risk or Systemic Risk: this is the risk that the whole market falls. You can’t diversify this risk away by investing in the market. You can address this risk by having some assets outside the market, in cash, in the money market, CDs, Bonds, real estate (tangible) etc. This risk relates closely to the timing risk which is next. If you have all your money in the S&P500 and it falls by half, but you don’t need anything from your account for 10 years, this market risk is not going to affect you. If you are retired and you have all your money in an S&P500 index fund that yields 1.9% and you’re taking 4% from your account, you might have problems.

Time – Stock investments fluctuate in price for many reasons. Some make sense – some don’t. What if you invest money in the stock market for your retirement and you think you will retire in six years? Is that enough time to have money in the market? Probably. What if you unexpectedly get retired in two years and you need to start withdrawals sooner than later? The timing change may have a significant negative impact.

Emotions – In my experience, this is what causes most investment failure and underperformance, not stocks that go bankrupt. We are wired to make decisions based on self-preservation. This wiring causes us to want to make the exact opposite of the right decision in many instances relating to investments. I’ve bought and sold lots of stuff over the years. The basic idea was to buy something for a dollar and sell it for two dollars. This started with stocks at 16, books from 18-25, cars from 21-26, real estate from 23-26, most recently privately held businesses. The most profitable efforts all had a couple of things in common: You need cash available to take advantage of opportunities when they arise. You need to be open to opportunities others are ignoring. You need to be willing to commit significant amounts of time to learn about new things. You need courage to do something no one else wants to tackle. Consistently the mistakes I have made and the ones I have seen others make in business and in the stock market usually have an emotion tied to them. Greed holding out for too much, fear of selling at the wrong time or being unwilling to buy. To make good decisions about business and investing requires being able to view options and decisions without emotion. This is harder than it sounds. Part of our job at Threadgill Financial is to help take the emotion out of investment decisions for you.

This notion that we are our own worst enemy when it relates to investments is well documented. Check out this graphic from Richard Bernstein mapping out various asset class returns from 1993-2013.

This data offers strong support for the idea of buying quality assets and leaving them alone. On the other hand the price you pay for that asset has a LOT to do with how much return you make. If you invest at the top of a market cycle your returns will probably be worse than if you buy lower. -Zac